Read More

How young people can buy

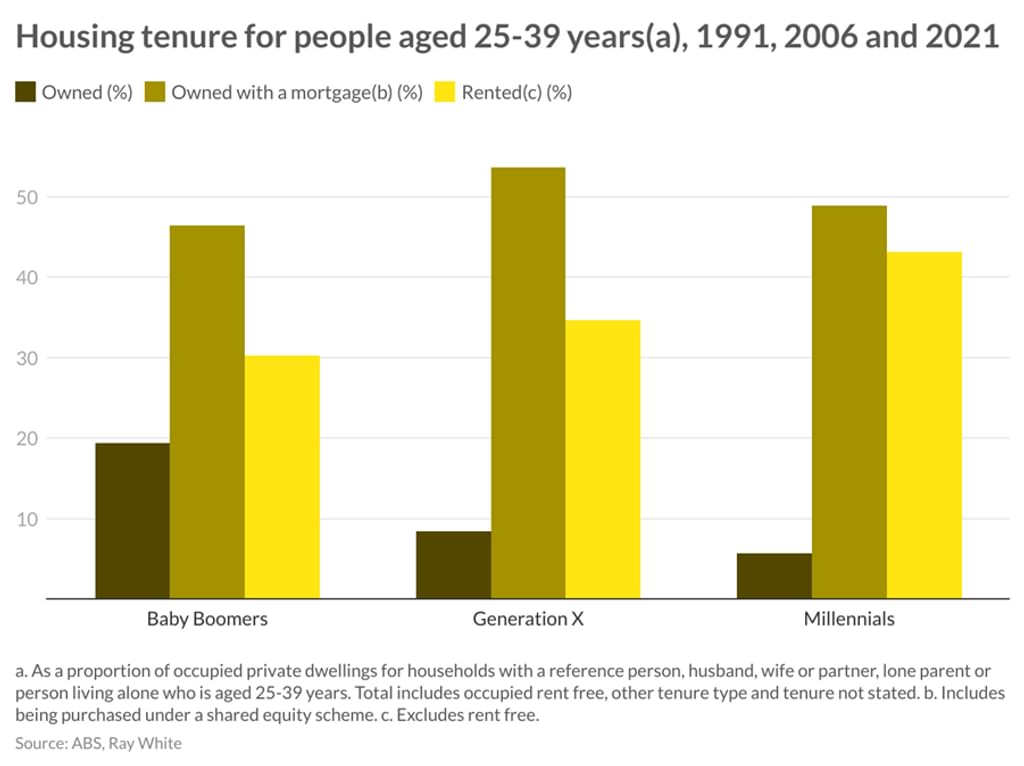

This demographic shift in home ownership may be representative of the fact that many young adults today are priced out of their capital city markets.

In 1991, owning a capital-city home was achievable for many young adults as more affordable housing meant many could save up for a deposit by the time they were ready to move out of their parents home and start a family. Today, in a much less affordable market and a challenging purchasing environment, many young adults that are ready to buy their first home may be hesitant as they are priced out of the capital-city market they’re living in.

As it’s now more difficult, owning a home in a capital city will require a different mindset than what our grandparents had in the late 20th century. It will require a greater appetite for risk and patience. Strategic planning has become essential for the longer journey many of us will have to take in order to own a capital city home.

Rentvesting has become a popular way for young-adults to get their foot onto the property ladder. Interestingly, in the past year, over 50 per cent of property investment purchases were made by Millenials and Gen Z, according to data from the Commonwealth Bank. This is a strategy where a buyer purchases an investment property in a more affordable area while renting in the suburb in which they would like to live. The capital gain made on the investment property can ultimately assist with the purchasing power of the young adult when they are in a position to purchase a property in their desired location. Importantly, “rentvestors” get a foothold in the real estate market, and minimise any disadvantage caused by a continued increase in home prices.

Ultimately the success of rentvesting to grow purchasing power, depends on the ability for your property to grow in value and earn rental income. There exists a trade off between the two and while there may exist some properties that lie in the “sweet-spot” of the two benefits, often we see that strategically buying properties in suburbs that maximise one benefit can be the most effective strategy.

1. Do you go for capital gains?

This strategy involves buying in a suburb that shows promise for significant capital growth. So when it comes time to sell, the difference between your purchase and selling price contributes to narrowing the gap between your budget and the price of your desired home in your capital city.

2. Or, do you go for high rental yields?

This strategy involves buying in suburbs where the rental yield is high, maximising the cash flow from the property investment. This strategy is attractive for potential investors who prefer more reliable income returns and seek to use this additional cash flow to build savings that will, in turn, assist their ability to purchase their desired future property.

The key to choosing a strategy requires an adequate understanding of trends driving those suburbs which are currently seeing the greatest financial returns; be that of capital gains or rental yields.

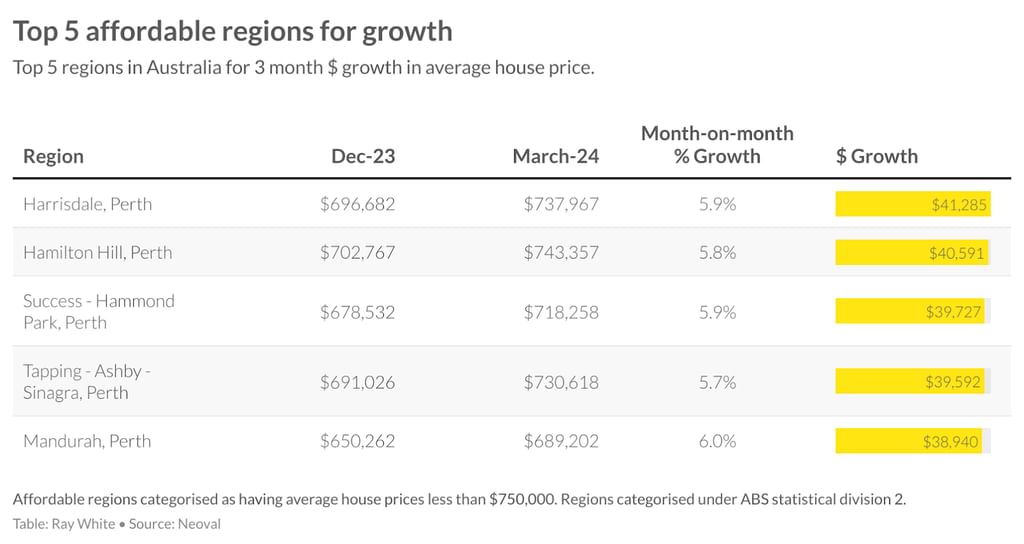

We look closely at those suburbs that are at the beginning of a potential medium-term price appreciation cycle and which may be suitable for ‘capital gains investors’. We consider those suburbs that have experienced the highest three month house price growth, and investors might find it attractive to invest into on the basis that they have momentum for further appreciation. Note that although they have experienced strong capital growth in the short term, it doesn’t necessarily mean that they will continue to do so. This is one of the difficult parts of choosing a property based on its potential for capital growth.

The top five regions in Australia for three month growth in average house prices are in Perth which has been a particularly strong market over the past two years. Will this growth continue to be strong?

It is difficult to predict, however, there have been several factors that are contributing to this growth. Partly it’s population growth which has been reasonably strong. A second factor has been growing wealth from increasing demand for green energy minerals. A third factor has been rising construction costs – building a new home in Perth is now a lot more expensive than it was prior to the pandemic. This has meant that homes built several years ago are looking like good value given the cost to build a similar home is so much more expensive.

Harrisdale in Southern Perth, tops the list recording a $41,285 (5.9 per cent) growth in house prices since December. Hamilton Hill is a close second growing in value by $40,591. Demand for Perth’s affordable housing is the highest in Australia for any niche property market. Specifically, the LGA of Armadale, where Harrisdale is home, tops the nation for lowest median days on market, recording eight days for house sales in the past 12 months. As Perth is also Australia’s fastest growing city in terms of population, these affordable southern pockets of Perth seem to provide the greatest opportunity for “reinvestors” to maximise potential of capital gains.

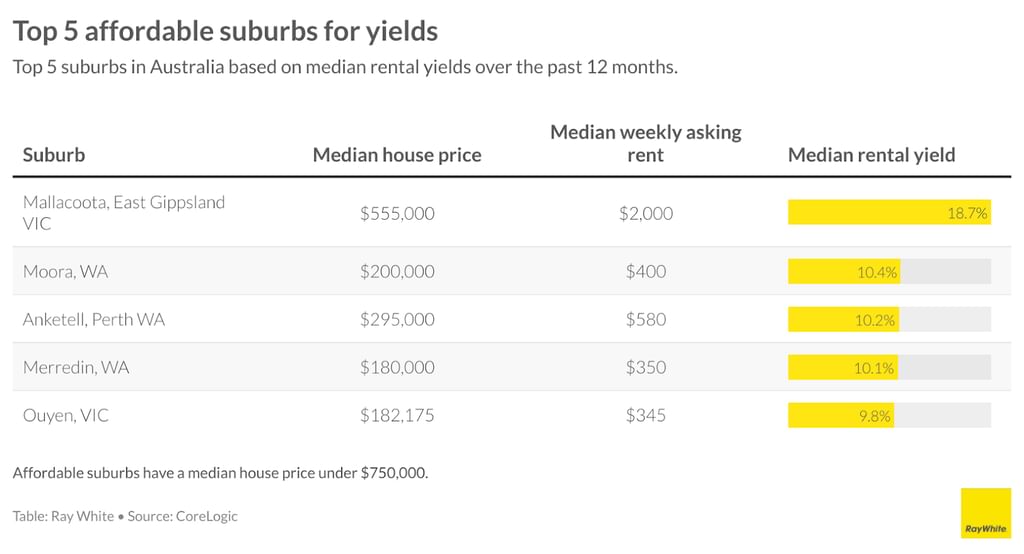

For the “high yield investor”, the major trend we’re seeing between suburbs with high yields are those mining towns where nearby mines and power stations generally employ 50 per cent of the local population. The growth in Australia’s mining industry, both in size and earnings, has meant property owners in these isolated mining towns have seen strong rental demand and rent growth. While this is the case, investors must be aware of the volatility of this industry and the historical challenges that investors have faced when mining conditions change. They are riskier suburbs for investments as rental income and are generally not advised for first time investors.

Excluding volatile mining towns, there is less of a defined trend. Generally areas with very low incomes have high yields but do not see strong capital growth. Currently, Mallacoota in East Gippsland Victoria tops the nation, recording a median rental yield on house rentals over the past 12 months at 18.7 per cent, likely due to a lack of rental properties in the town.

Overall however, there seems to exist no real trend between the top five yielding suburbs. Mallacoota is a seaside town popular with tourists, whereas the rural town of Moora has seen rental yields driven by a slow down in house price growth.

Rentvesting has its risks, as does any investment, and so potential buyers must consider what factors are most important in their purchasing decisions and consider seeking professional advice to navigate through their first purchase. Capital gains tax, the inherent risks of leasing your property, and uncertainty of property price growth should all be considered in determining where and when you should step into the market. Importantly, given the above analysis, doing research into the suburb that you would like to rentvest in is critical.

On a whole, it seems that with historically low vacancy rates, possibilities of interest rate cuts and high population growth, the Australian capital-city property market will continue to be harder for first-home buyers to get in. Rentvesting is one way to live in an expensive city but invest in property in a much more affordable area.

Jemima White | Data Analyst Ray White Corporate